Over the past years, among the many things technology has transformed and continues to do, it is revolutionising the way we bank and access banking services. As the internet opened access to a tremendous amount of information, financial technology is also making banking more accessible, more responsive, and more secure. As a millennial bracing for risky ambitions, higher costs of living, heavier financial commitments, and delayed retirement, could fintech be the money messiah I have been looking for?

It’s expensive being a millennial in Singapore

We face burgeoning costs of living for essential goods, but also desire creature comforts at the same time. Many of my friends have Dyson vacuum cleaners that cost almost $1K. Some of us don’t boil our water anymore because we now have water dispensers that somehow has WIFI capabilities. Maybe it’s a case of my own subjective perspectives, but regardless, it’s true that there are very real challenges (and often expensive) people like me have to overcome.

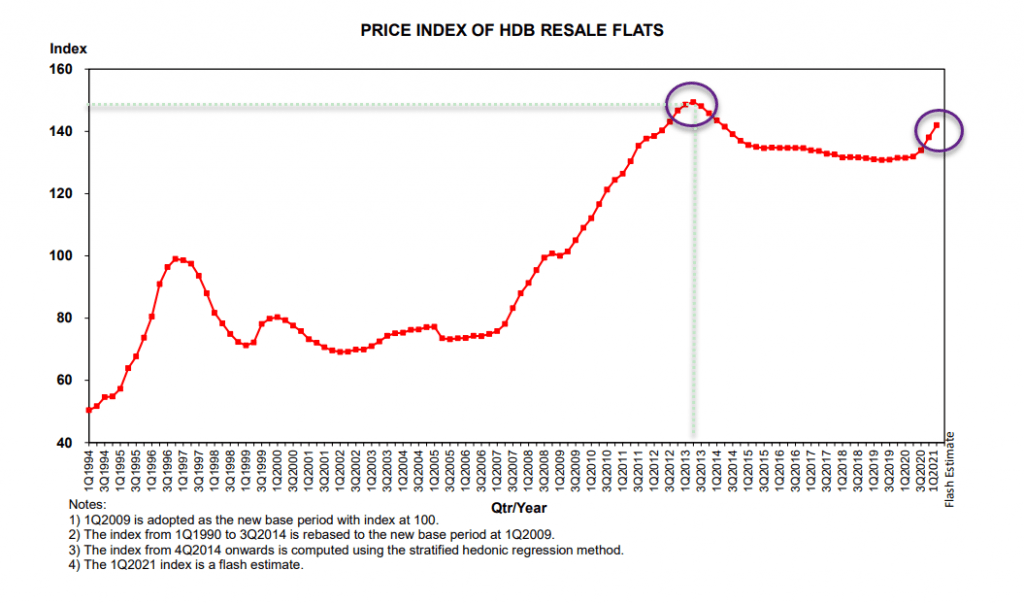

Trying to stay cool-headed over hot property prices

I’ve always dreamed of living atop a hill, just not a price hill. | Source: Property Investor Insights

Public housing is in such high demand that every couple needs to plan years ahead waiting for their flat that costs half a million to be ready. If they cannot wait, or if the combined income exceeds the income ceiling, they face record-high prices in the resale flats market and potentially not qualify for some housing grants. Some will not be thrilled either that the other option is to buy ECs that often cost >$1 million.

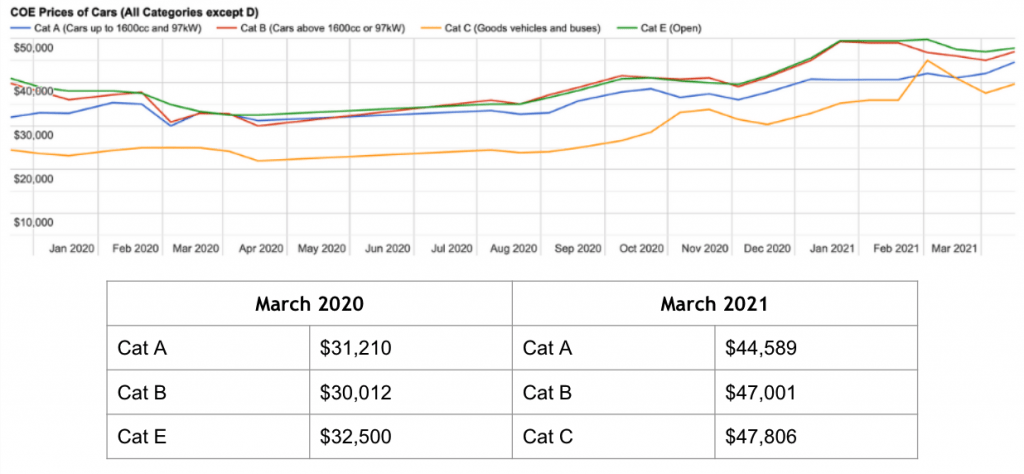

Rising car costs

The cost of owning a car is being…driven up. Haha. | Source: Carro

I’d be surprised if a young adult’s financial planning doesn’t factor in possibly owning one. To buy one of Singapore’s most common cars, the Honda Civic, you have to fork out about $127k the moment you drive it out of the showroom. And don’t forget that COE prices are still rising, as well as fuel costs.

Technology can be costly too

As our lifestyles become more and more digitalised, our thirst for data and connection speeds means we are paying more to work, communicate and be entertained. Choosing not to keep our tech gadgets up to the times is no longer an option; we are sometimes forced to spend on new tech.

We can benefit greatly from better banking

Of course, this is not to say we should start a family under a bridge, ride bicycles everywhere and buy homing pigeons to send text messages. The expenditures stated above are to most of us living essentials. Earning more money is only ⅓ of the equation; the ⅔ includes keeping more of our earnings and generating more with it.

Having a banking service that we can rely on to seamlessly facilitate our spending WHILE covering our future backsides, i.e. saving on our behalf and growing our wealth without us having to micromanage it, is so coveted. In my opinion, the banks do offer a suite of tools to do that, but it’s still quite a tedious and complicated process that could do with greater transparency.

My cost of banking is reduced

As a customer of one of the major banks here, I must maintain a minimum balance of $500 in my account (which is virtually loaning the bank at interest rates way lower than that of inflation) and pay $2/month as a service charge. My credit card comes with a $200 annual fee and God forbid I forget to pay my bills lest I get slapped with a 27% finance charge.

Me whenever it’s credit card bill payment time.

Nowadays, fintech firms like Hugo issue their own cards that are way more flexible, user-friendly and convenient. Some ways I saved on banking costs:

- I haven’t paid any fees for maintaining my Hugo Account because there isn’t any,

- I didn’t have to maintain any minimum balance nor pay fall-below fees,

- My Hugo Card charges zero admin fees, and

- I can use all of Hugo’s features regardless of my annual income or employment status.

Now, my bank account is mostly for salary crediting and for official matters. I have moved almost all my spending to Hugo and virtually removed the risk of incurring fees on late card bill payments. My next step is to disable some of my bank cards and save >$200/year.

Investment apps helped me lower the costs of trading

With way lower overheads than banks do, fintech platforms can offer pretty competitive rates. Let’s take gold investment for example. Investing in gold via a bank can be rather costly. Banks in Singapore typically charge

- Annual holding fees (about 0.25% p.a.) that recurrently eat into your holdings,

- A one-time admin fee at a few dollars per trade, thus increasing your cost of trading.

It’s really not worth it if I am planning to buy only a small amount, and these fees can rack up as my gold holdings increase. Banks require us to buy a minimum amount of gold each time too.

Hugo’s Gold Vault allows me to

- Buy gold at ANY amount.

- Charges only a ONE-TIME 0.5% admin fee per trade and nothing else beyond that. This makes the cost structure very flexible and fair for me instead of a flat fee.

- I don’t have to incur time and opportunity costs by having to go to a bank to do my trade. I can set a gold-buy schedule in the app anywhere and at any time.

I set up a monthly $100 gold-buy schedule so I can build up my gold holdings over time steadily. I’ve been paying no fees during the free trading period that ends on 27 November 2021.

Since using Hugo, I have accumulated nearly 10g of gold (worth about $750) at the time of writing and I only paid about $3.75 in fees so far, which is WAY LESSER than what I would have paid if I had gone the bank route. It easily becomes a non-issue when my gold holdings appreciate in value; I can recover those fees in no time. Hugo is working on including more investment products in the near future, offering the same affordability and convenience.